Inside Volatility Trading: The Constant Change of Volatility

Kevin Davitt

▬

May 4, 2021

Spiders and the webs they weave

Out of sight among the eaves

Of the house we live in solid made

That holds the lives we choose to lead

Mountain Man - AGT

In classes and other client engagements, the Options Institute will often point out that volatility is one of the most misunderstood topics in capital markets. The term itself has a powerful connotation that typically runs independent of the word’s denotation. That dichotomy between the term’s definition and how it’s (typically) interpreted presents opportunity and risks.

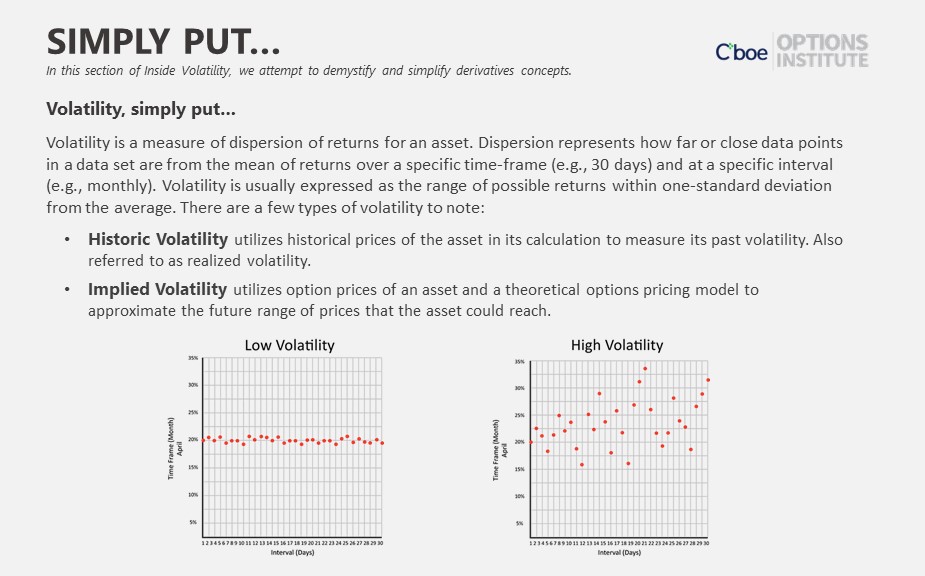

Volatility references the range of price changes in an underlying security, commodity, or index over a defined time horizon. Volatility is how we quantify the speed and magnitude of moves in the market. It is “a statistical measure of the dispersion of returns for a given security or market index over a given period of time” (Investopedia) and is typically based on closing values for the underlying. Volatility is a relative measure of change.

For example, 20-day historical volatility (closing) for the S&P 500 Index was 10.6% as of April 27.

For more on how one arrives at that number, I encourage you to read this week’s Simply Put.

Most people don’t think of volatility as a calculation because in “everyday life” volatility has a spontaneous nature, one associated with negativity because we’re unprepared. Volatility is more closely associated with poor outcomes as opposed to standard deviations. It would be unusual to hear someone say, “I hope to introduce significant volatility into my day.”

Nevertheless, change is a constant whether you’re referencing capital markets or life in general. As such, volatility is too. The rate of change can fluctuate dramatically but change is as persistent as time.

Daily changes in the broad market have been relatively insignificant of late, and historical volatility measures have waned. For the month, on average the S&P 500 Index has moved only 58 basis points (bps) per trading day (data thru April 27). That compares to 84 bps for the month of March, 62 bps in February and 80 bps in January.

S&P 500 Index Average Daily Change in Basis Points (BPS)

The visual above illustrates the average ebb and flow of daily changes in the S&P 500 Index. The long-term historical average for the broad market is ~73 basis points per day. The last +/-2% day (200 bps) in the broad market, considered a volatile session, was March 1. There have been only four sessions thus far this year with +/-2% changes or greater. For full year 2020, there were 44 such volatile sessions; the S&P 500 Index experienced a 2% move up or down 17.5% of the time. This year, the broad market has had 2% swings on only 5% of the trading days.

On a related note, as the S&P 500 Index grinds higher with diminished velocity, the VIX Index® has been measuring lower with each subsequent S&P 500 Index high. The Goldman Sachs research team put out the visual below and drew comparisons to the 1998 period of new highs for the market.

Closing Level of S&P 500 and VIX Indices on Each Date of New All-Time S&P 500 Index Highs

In August of 1998, Russia defaulted on debt issues and devalued the Ruble. That unlikely event triggered significant macro volatility. Long Term Capital Management - a Greenwich, CT-based hedge fund with a previously stellar track record - was wiped out in the wake of the Russian currency chaos.

It’s no secret that I have a genuine affinity for history and particularly market history. Dean Curnutt, CEO of Macro Risk Advisors (MRA) likely shares my historical fondness. The firm provides global market risk analysis and execution services for institutional clientele. MRA recently published their “25 Sayings on Vol and Risk.” Here are a few that stood out to me:

- If history is a foreign country, the history of risk is another planet.

- When it comes to appreciating risk, investors seem to suffer from amnesia. Past, well documented risk events are deemed irrelevant as useful analogues to present market vulnerabilities.

“The Go-Between” by L.P. Hartley was published in the early 1950s. The work centered on a “naïve” 13-year-old whose view of the world is altered as he reads a diary from decades earlier. The book includes the quote: “the past is a foreign country; they do things differently there.”

To what extent are things done differently here and now?

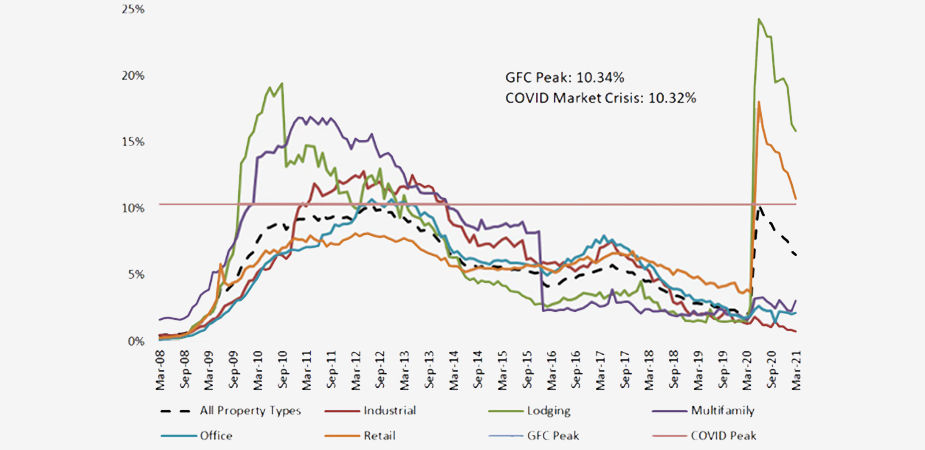

After reading the MRA application to volatility, I thought about a recent Intercept article and podcast. The column and related podcast address potentially problematic behavior in the Commercial Real Estate lending markets. Even casual market observers know that the relaxed lending standards for residential real estate buyers played a role in the 2008 financial crisis. Huge pools of mortgage-backed securities were created. Many were sold as AAA rated bonds after being reviewed by the ratings agencies. Delinquencies became widespread as homes lost value and buyers were unable to refinance. Thus, systemic risk became a real concern.

The housing market collapse was unique when compared to the exogenous shock like the Russian default or a novel virus that impacted trade and asset values. The seeds for the 2008 volatility were sown for years. The true risks were obscured by rising home prices and availability of capital. The Intercept article quotes Warren Buffett who said, “it’s only when the tide goes out that you learn who’s been swimming naked.”

Has a degree of collective amnesia beset the markets?

“It is difficult to get a man (woman) to understand something when his (her) salary depends on their not understanding it.”

Upton Sinclair

Is it possible that history may “rhyme” in the wake of the COVID-19 crisis?

Perhaps it’s too soon to grasp the full impact the virus will have on the Commercial Real Estate market, but it’s difficult to believe it won’t be meaningful. Will the value of commercial properties decline significantly because of the pandemic? Will the tenants of those commercial properties be able to service the monthly payments? Will the securities tied to the performance of those properties be downgraded? What impact might that have on global equity markets?

Time will tell.

Commercial Mortgage-Backed Securities (CMBS) Delinquency Rates

"Price is a liar" (John Burbank, Passport Capital)

"A price is simply where two counterparties managed to transact. Look no further than what VaR models told investors about portfolio risk in late 2006 as the VIX Index dipped below 10 even as an epic tidal wave of portfolio deleveraging was in the process of building."

MRA 25 Sayings on Vol & Risk

This market truism reminded me of the last Inside Volatility piece. The crux of the previous writing was that prices and sentiment tend to be transient and often disconnected from value. Prices can (and do sometimes) change quickly, but value is more impervious.

It’s possible that some asset prices and true value have become disconnected. It’s also conceivable that prices are simply reflective of an improving macro backdrop and the uncertainty that hung over much of the past year will give way to a halcyon era. Perhaps the combination of easy fiscal and monetary policy didn’t just pull forward demand. Maybe it’s here to stay.

Time will tell.

Exposure & Hedging

Securities have linear price properties. Granted, equities and ETFs can move higher/lower with differing velocities, but the exposure profile is 1:1. In other words, for every $1.00 move higher or lower, the holder makes or loses $1.00. Options have a more nuanced exposure profile as a function of their embedded convexity. Options provide non-linear exposure.

Gamma is the second derivative of delta and they both play a role in the non-linear payout. So, too, do potential changes in implied volatility expectations. The stampede of interest in OTM options (mostly calls) on momentum names in 2020 and early 2021 was a collective clamoring for convexity.

VIX options are some of the most active in the market in part because of their potential hedge utility and their potential convexity. For example, on January 27, 2021 the S&P 500 Index fell by 2.6%. The VIX Index moved from 23.02 to 37.21, gaining more than 60% close-over-close. On the same day, the March VIX futures (front contract NOT including Weeklys) closed at 33.05 after having settled at 25.30 the previous session. That was a 30.6% gain on the day.

The March contract still had three weeks until expiration at that point. The first weekly future (7 days to expiration) moved from 24.65 to 33.65. The weekly options would have the greatest convexity in that scenario. The March (standard) options would have also exhibited significant convexity.

The research below via Morgan Stanley is dated (2015), but illustrative. While it depends on the prevailing volatility regime and tenor, VIX options may offer a superior hedge vehicle if your concern is a sharp pullback in the short term as a result of their convexity.

VIX Index Screens Better for Large Gap Risks on Current Pricing

Current Premium Spent to Hedge $1,000,000

Here & Now

At the moment, the “price” (level) for the S&P 500 Index is well above its two-year (monthly) moving average. In fairness, historical averages have been skewed by the vicious selloff in early 2020. In the Inside Volatility report from early April, we showed how one-year realized volatility measures for the S&P 500 Index were falling dramatically because those measures no longer accounted for the huge swings in mid-March of 2020.

The two-year average shown below would still include the early pandemic period which pulls the average “price” calculation down. In any event, the S&P 500 Index is roughly 27% above that long-term moving average. The last time the S&P 500 Index was measuring at this premium relative to the 24-month moving average was February of 2018.

Deviation Above/Below Long-Term Mean (24-Monthly Moving Average)

Shifting the focus slightly, the rate of change for investment funds has been very volatile since the U.S. elections last November. According to research from Bank of America, global investors have funneled more capital into the market over the past five months than they did over the previous 144 months in total. That’s stunning and goes a long way in explaining the 28% rally in the S&P 500 Index since the end of October. The Euro STOXX 50 Index is up 40% over the same time frame. The MSCI Emerging Markets Index (MXEF) has gained 24% since November. MSCI’s EAFE Index (MXEA) is up 29% in the last five months

Inflows to Global Equity Funds Over the Past Five Months Exceed the Prior 12 Years

Let’s do the math a little differently. Between October 2008 and October 2020, on average, global investors allocated $3.14 billion per month into equity markets. Between November 2020 and the end of March 2021, global investors allocated $113.8 billion per month into equity markets. In November 2020, more than $91 billion flowed into U.S. listed ETFs alone!

Changes…

Change is ongoing. Trees in my area have gone from barren to full over the last few weeks. Roughly 40% of Americans have received at least one dose of a COVID vaccine. Home values are moving up (+17% year-over-year) and selling at the fastest clip in 15 years. If you’re interested in more esoteric opportunities in “virtual real estate,” there’s a non-fungible token (NFT) market available. More than $4 million in virtual land sales were consummated in March. Agricultural commodities are at multiyear highs and inflation is becoming a hot topic again. The Federal Reserve’s balance sheet has been expanding too. It holds ~$7.8 trillion in assets or 36% of nominal U.S. global domestic product (GDP).

Not everything is climbing. Forward-looking volatility measures, including the VIX Index and tradeable VIX futures, have been declining. Once again, volatility just is.

Finally, a very happy birthday to my mom. You’ve given me roots, wings, and love for the written word. You taught me that “the mind once expanded never returns to its original size.” THANK YOU.

And as we all play parts of tomorrow

Some ways we’ll work and other ways we’ll play

But I know we can’t all stay here forever

So I’m gonna write my words on the face of today

Blind Melon - Change

Volatility News

- Cboe Europe Derivatives Secures Support of Key Participants for September 2021 Launch

- Cboe Expands Product Suite, Geographic Reach

- Reuters: Coinbase options launch draws robust volume

- Interactive Brokers: Understanding Special Exercises and Pin Risk

- Bloomberg: A Volatility Quant Nets $540 Million as Momentum Trades Boom

- MarketWatch: Want to increase your dividend income? The strategies of these funds can help you do it

- Schaeffer’s Market Mashup: Covid-19 One Year Later — 365 Days of Volatility

Events

- May 6: Phillip Futures & Cboe - Introducing Mini VIXTM Futures: Characteristics, Market Conditions, Strategies for Capital Protection and Income Generation

- May 12: Demystifying the Option Greeks

- Webinar Replay: Introduction to the VIX index and How Investors Can Use It

Volatility411

Get the Inside Volatility Trading newsletter directly in your inbox by signing up here.

The information in this article is provided for general education and information purposes only. No statement(s) within this article should be construed as a recommendation to buy or sell a security [or futures contract, as applicable] or to provide investment advice. Supporting documentation for any claims, comparisons, statistics or other technical data in this article is available by contacting Cboe Global Markets at www.cboe.com/Contact.

Past Performance is not indicative of future results.

Futures trading is not suitable for all investors, and involves the risk of loss. The risk of loss in futures can be substantial and can exceed the amount of money deposited for a futures position. You should, therefore, carefully consider whether futures trading is suitable for you in light of your circumstances and financial resources. For additional information regarding futures trading risks, see the Risk Disclosure Statement set forth in the Risk Disclosure Statement set forth in Appendix A to CFTC Regulation 1.55(c) and the Risk Disclosure Statement for Security Futures Contracts.

This e-mail has been sent to you because you: 1) are a current or former subscriber to cboe.com; 2) have requested information from Cboe in the past; or 3) have been identified as an investment professional with interest in the subject matter.

Cboe®, Cboe Global Markets®, CFE®, Cboe Volatility Index®, and VIX® are registered trademarks and Cboe Futures Exchange™ and Mini VIXTM are service marks of Cboe Exchange, Inc. or its affiliates. Standard & Poor’s®, S&P®, S&P 500®, and SPX® are registered trademarks of Standard & Poor’s Financial Services, LLC, and have been licensed for use by Cboe Exchange, Inc. All other trademarks and service marks are the property of their respective owners.

Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of "Characteristics and Risks of Standardized Options." Copies are available from your broker or from The Options Clearing Corporation at 125 S. Franklin Street, Suite 1200, Chicago, IL 60606 or at www.theocc.com.

© 2021 Cboe Exchange, Inc. All Rights Reserved.

Related Posts