Nine Key Features of the Russell 2000 Index and New Mini-Russell 2000 Index Options (MRUT), Part 2

February 17, 2021

Cboe is launching Mini-Russell 2000 Index options (ticker: MRUT) on Monday, March 1, subject to regulatory review. In anticipation of the launch, we’ve compiled a list of nine features that may help investors better understand the Russell 2000 Index and the new Cboe Mini-Russell 2000 Index options. This is the second post in a three-part series. Read about the first three features, here. Features 4-6 are below.

Understanding the Small Cap Market

The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity market. At the end of 2020, the Russell 2000 Index reached record numbers, based on promising news about the COVID-19 vaccine, which indicated a potential boost to sectors of the market that are more sensitive to economic recovery, such as travel, energy, retail and industrials.

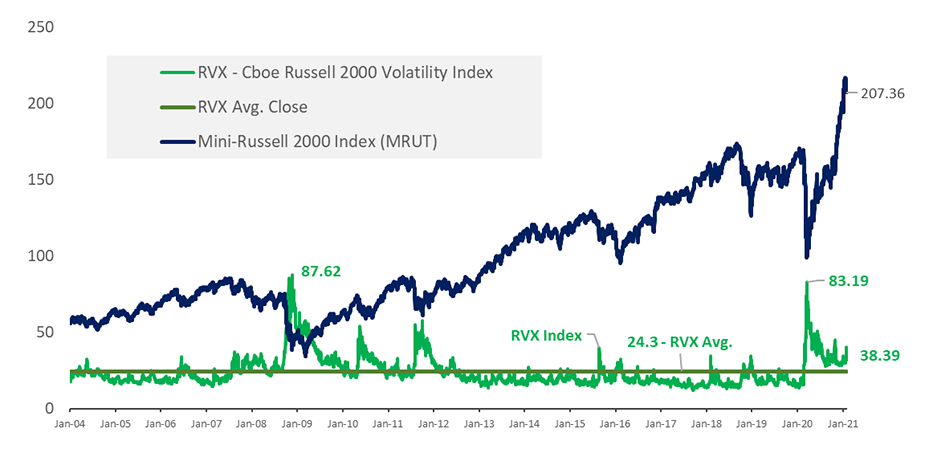

4. Higher Volatility, Negative Correlation and Collar Strategies

Overall, small-cap stocks tend to be more cyclical and more volatile than large-cap stocks, as well as more sensitive to improvements in the economic cycle. The Cboe Russell 2000 Volatility Index (RVXSM) provides an estimate of the expected 30-day volatility of Russell 2000 Index returns and uses the values of options on the Russell 2000 Index in its calculation. Below are some recent observations of the RVX Index:

- Higher Volatility Over the Past Year. Between February 2020 and January 2021, the average daily closing value for the RVX Index was 37.3 -- 13 volatility points higher than its long-term average of 24.3 since January 2004. On March 16, 2020, as worldwide economies began shutdowns in response to the COVID-19 pandemic, the RVX Index closed at 83.19, its highest daily closing value since 2008.

- Higher Volatility than Other U.S. Indices. From February 2020 through January 2021, the average daily closing values for key volatility indices were 37.3 for the RVX Index, 33.9 for the Cboe Nasdaq Volatility Index (VXNSM), 30.2 for the VIX® Index and 30.1 for the Cboe Dow Jones Industrial Average Index (VXDSM).

- Negative Correlation. The daily returns of the RVX and Mini-Russell 2000 indices had a correlation of -0.71 since January 2004. Expected volatility and index options prices often surge as stock indices tumble. In market regimes with higher volatility, Mini-Russell 2000 options hedging strategies may appeal to risk-averse investors, while Mini-Russell 2000 option income-enhancement strategies may appeal to income-oriented investors.

Small Caps: Volatility and Stock Indices

There was a -0.71 correlation in the daily returns of the Cboe Russell 2000 Volatility Index (RVX) and Mini-Russell 2000 Index (MRUT)

Daily closing values, January 2, 2004 - February 2, 2021. Source: Cboe Options Institute

5. Higher Options Premium Collected for Option-Writing Strategy

Income-oriented investors face new challenges, as the yields for “traditional” investments related to some major stock and bond indices have fallen substantially over the past 35 years. Investors often use option-writing strategies to receive options premium with a goal of gaining higher yields, particularly in times of above-average volatility.

The chart below shows the gross premiums (as a percentage of the underlying index) that were generated by two Cboe benchmark indices that track option-writing strategies, The Cboe Russell 2000 BuyWrite Index (BXR℠) and the Cboe S&P 500 2% OTM BuyWrite Index (BXY℠).

- The Cboe Russell 2000 BuyWrite Index: A benchmark index designed to track the performance of a hypothetical covered call strategy that holds a long position indexed to the Russell 2000 Index and sells a monthly at-the-money (ATM) Russell 2000 Index call option.

- The Cboe S&P 500 2% OTM BuyWrite Index: A benchmark index designed to track the performance of a hypothetical covered call strategy that holds a long position indexed to the S&P 500 Index and sells a monthly out-of--the-money (OTM) SPX call option.

Monthly Gross Premiums: Option Writing on U.S. Indices

May 2006 - January 2021. Source: Cboe Options Exchange, Inc.

The BXR Index generated higher gross premiums than the BXY Index for two reasons. First, the BXR writes ATM calls and the BXY writes OTM calls. OTM call option-writing strategies often generate less premium but may have more potential for upside moves in a bull market regime. The chart shows gross premiums, meaning the net returns for the BXR and BXY may be less than the gross or negative. The BXR Index has generated average gross premiums of 2.2% per month since May 2006. In the last 12 months the BXR Index generated average gross premiums of 3.4% per month. Second, the aggregate of gross premiums generated by the BXR Index over the past 12 months was 40.9%.

6. Potential for Lower Volatility for Certain Mini-Russell 2000 Index Options Strategies

Put-selling strategies are often believed to come with excessive risk, but the chart below shows that’s not always the case. The Cboe Russell 2000 PutWrite Index (PUTRSM), which holds Treasury bills and sells cash-secured Russell 2000 put options, had a less severe maximum drawdown than four other indices.

Most Severe Drawdowns Since 2001

Past performance is not indicative of future returns. January 2001 - February 2021. Sources: Zephyr and Cboe Options Institute.

More Strategies to Explore

Collar Strategy Using Mini-Russell Index Options

Options collar strategies may help market participants hedge downside risk and lessen volatility with minimal cash outlay. The Cboe Russell 2000 Zero-Cost Put Spread Collar Index (CLLR), tracks the performance of a hypothetical strategy that holds Russell 2000 stocks, buys RUT put options spreads, and sells RUT call options. Over the past 20 years (January 31, 2001 to January 31, 2021), the annualized standard deviations were 15.9% for the CLLR Index and 19.6% for the Russell 2000 Index.

Buy-write Strategies Using Mini-Russell 2000 Options

Buy-write strategies have the potential to generate gross premiums on a regular basis and may help dampen portfolio volatility.

Cash-secured PutWrites Using Mini-Russell 2000 Index Options

The historical performance of a cash-secured put-write strategy that uses Russell 2000 Index options shows lower volatility and improved tail risk, which may appeal to risk averse investors.

The Wilshire Associates whitepaper, The Cboe Russell 2000 Option Benchmark Suite - Improving Diversification by Harvesting Volatility Risk Premiums (2020) analyzes the performance of these indices and strategies. Download a copy.

Learn More

- Cboe Mini-Russell 2000 Index (MRUT) Options

- Mini-Russell 2000 Index Options Fact Sheet

- Mini-Russell 2000 Index Options Contract Specifications

- Wilshire Associates Whitepaper: The Cboe Russell 2000 Option Benchmark Suite - Improving Diversification by Harvesting Volatility Risk Premiums

- Fund Evaluation Group Study: Evaluating Options for Enhanced Risk-Adjusted Returns: Cboe Russell 2000 Option Benchmark Suite and Case Studies on Fund Use of Options

Related Posts